Note to Readers: Although this story revolves around changes to particular Medicare health insurance plans, the lesson it offers is universal. During open enrollment, don’t just automatically renew your old plan. Look for changes your insurer is implementing in the coming year in the Annual Notice of Changes and see if a different plan may better suit your needs.

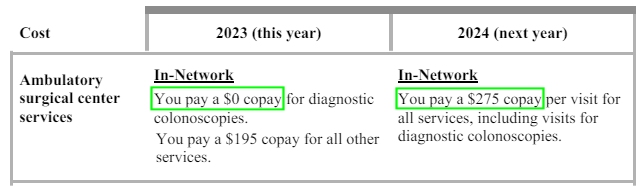

Here’s an example of a nasty change by Arkansas BlueMedicare. Their Premier Choice advantage plan used to provide free diagnostic colonoscopies, but for 2024 they added a $275 copay.

*MOUSE PRINT:

A very popular Medicare Part D drug plan is Wellcare Value Script (PDP). This is optional coverage for those with original Medicare whether or not you also have a supplement (medigap) plan. (Original Medicare does not cover drugs so many seniors buy a separate drug plan called Part D.)

A reason it is so popular is that it tends to be the cheapest plan in some states. For 2024, for example, in Massachusetts, Maine and perhaps elsewhere, the monthly premium is only 50 cents! In some other states it is zero!

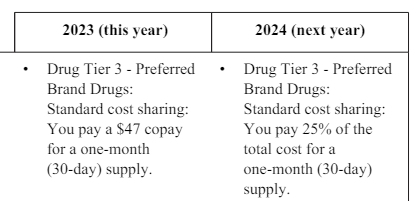

It does have the maximum allowable deductible — $545 — but beneficially it does not apply to tier 1 or 2 drugs. Tier 1 has no copays, and tier 2 is only $5 or $15 for 30 or 90 days, respectively. But there is a big change for tier 3 drugs.

*MOUSE PRINT:

For 2023, there was a flat $47 or $44 copay for tier 3 drugs. That means whatever the full cost, you only had to pay forty-something dollars.

But, for 2024, that changes to co-insurance. To MrConsumer, “co-insurance” is a dirty word. It is cost-sharing between you and your insurance company. They pay part of a particular bill, and you pay a certain percentage of it. For 2024, you will pay 25-percent of the full cost of drugs in the Wellcare plan for that tier. If it is an expensive drug, you could get soaked. If it is a cheap drug, you could save compared to 2023. Note that some other copays are lower for 2024 on this Wellcare plan.

Now it’s time for you to fess up.

The bottom line is EVERY YEAR you really need to check and compare the features and costs of your current plan with what various of next year’s plans offer. This goes for regular insurance plans and any of your Medicare plans — Advantage, Supplement, or Part D (drugs). Remember to also check the drug formulary for changes to what drugs are covered, in which tier they reside, and what any restrictions are.

I wonder if the prescription copay is for the “full” or “negotiated” amount and if it takes into account Rebates paid to Pharmacy Benefit Managers.

Good advice.

Sometimes I’ve had trouble getting drug costs from various pharmacies. For example, last year I wanted to refill a prescription with CVS Caremark and they told me that they couldn’t confirm the price (for a generic drug, no less) until I placed an order!

In that case, I went to my local pharmacy, which was able to give me a firm price in advance of my purchase.

I just have ‘regular’ Medicare & a drug plan that I pay $4.15 (but the price is going up to $4.50 next year) per prescription.

My AARP/United Healthcare “Walgreens” Prescription plan is going from $32 a month to $72 for reasons no one has been able to explain to me. At least UHC was nice enough to send me a warning letter. I have an upcoming phone appointment during the enrollment period with my Medicare counselor to pick a new one.

This is a really useful example. We’re did a lot of discussion about healthcare this year and on what plan to pick.

I would also recommend that people always compare their prescription prices to the GoodRX price.

I had a very nice phone discussion with a Humana advisor. The call lasted almost an hour, and he found me a Humana plan, similar to the one I already had, but better and cheaper.

I think it’s best to get an independent Medicare insurance broker not go to the insurance companies themselves. Mine brings out several plans from different companies for secondary and drug plans. And the changes in Medicare and secondary coverages from last to 2024. So far I’ve had better coverage for less than my neighbors who have called their insurance companies not a broker. But that’s been my experience for 5 years.

I have no choice. It is impossible to get a regular ppo self pay insurance policy in Massachusetts that is at all reasonable. The copays are insane. A drug like entresto you pay 250 they pay 50 for a month’s supply. The copays for labs and radiology are crazy. And the premiums horrendously high. Between the deductibles and copays and out of pocket maximums, it is mind altering. But as someone once said “insurance is like the mafia.” You pay them for protection against the chargemaster prices of high healthcare costs.

You need to move out of Taxachusetts!