When MrConsumer’s dentist advised him that a new cavity might be in its earliest stages of development, he checked out fluoride rinses that claim to restore minerals to weak spots in tooth enamel and prevent cavities.

When MrConsumer’s dentist advised him that a new cavity might be in its earliest stages of development, he checked out fluoride rinses that claim to restore minerals to weak spots in tooth enamel and prevent cavities.

The granddaddy of brands is Act, formerly owned by Johnson & Johnson, and recently acquired by a company called Chattem.

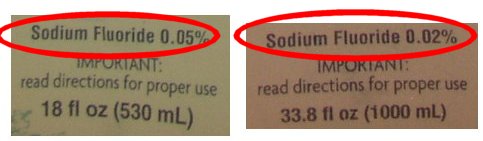

Act comes in two sizes: 18 ounce and 33.8 ounce. Luckily for MrConsumer, Rite Aid had the large size on sale last week, and there was a rebate. It was a seeming no-brainer to buy the big size.

Upon closer examination of the ingredients label, MrConsumer found a shocker:

*MOUSE PRINT: The larger bottle has less than half the strength of fluoride compared to the smaller one.

Now who would ever expect that a different size bottle would have a different strength of the active ingredient? In fact, if you look at the larger bottle, there is a “2x” on it. Without reading carefully, one might assume that “2x” means twice the strength or twice the size, but certainly never half the potency. A closer examination reveals that is says “2x a day”. Okay, so you can use the product twice daily.

As it turns out, the company says the smaller bottle is a once a day product, and the larger one is a twice a day product. Apparently you get the equivalent amount of fluoride using the diluted version two times a day.

Nonetheless, with such an inconspicuous but important difference, countless customers in the habit of using the product once a day may buy the large size, rinse as usual, and unwittingly not get the protection they expect.

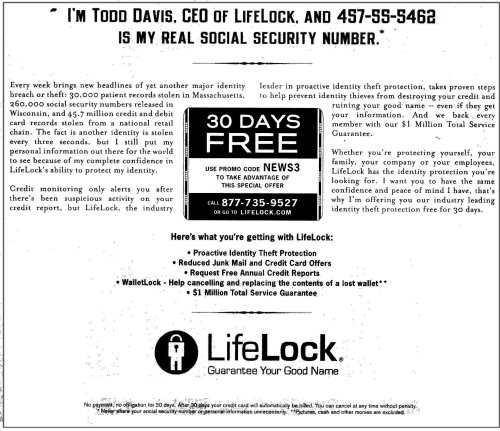

With stories about identity theft, stolen social security numbers, and compromised account information filling our newspapers weekly, no wonder a number of companies have sprung up to help protect you.

With stories about identity theft, stolen social security numbers, and compromised account information filling our newspapers weekly, no wonder a number of companies have sprung up to help protect you.