We are in peak shopping season now and that means scammers are working overtime to steal your hard-earned money.

One technique being used by some crooks is to take out Facebook ads using the genuine front page of a retailer’s circular like this spotted by Trend Micro:

When you click that ad or the “shop now” button you are taken to a site that looks like Big Lots.

Scroll down the ad.

*MOUSE PRINT:

In fact, it brought you to BigLotsClearances.com — a site made to look like the real Big Lots site. And if you scroll through some of bargains being advertised, the prices are impossibly low. An electric motor bike for thirty bucks – 90% off? And a canister of Tide Pods less than three dollars? We should be so lucky.

Before you click any Facebook ad, try to determine what URL you are going to be directed to by hovering over the clickable area with your mouse. Beware of look-alike/sound-alike website names. And if the deals on the actual website are simply too good to be true, get off that website quickly just in case it is booby-trapped with a virus.

The FTC and 17 states recently sued Amazon for using its monopolistic power to the detriment of its third party sellers, competitors, and customers.

Amazon uses a number of tactics to punish its own third-party sellers who offer lower prices outside of Amazon.

According to the complaint, the sanctions Amazon levies on sellers vary and can include:

*MOUSE PRINT:

Amazon knocks these sellers out of the all important “Buy Box,” the display from which a shopper can “Add to Cart” or “Buy Now” … Nearly 98% of Amazon sales are made through the Buy Box and, as Amazon internally recognizes, eliminating a seller from the Buy Box causes that seller’s sales to “tank.”

Another form of punishment is to bury discounting sellers so far down in Amazon’s search results that they become effectively invisible.

If a competitor lowers a price, Amazon often lowers its price to the penny to instantly blunt the competitor’s advantage.

Part of its plan to keep prices high involved a covert strategy called “Project Nessie” which the FTC says resulted in Amazon pocketing more than a billion dollars from American’s pocketbooks.

*MOUSE PRINT:

Project Nessie predicted the likelihood that the online store or stores offering the lowest price for a given product would follow an Amazon price increase. Armed with these predictions, [Amazon] increased products’ prices when those price hikes were most likely to be followed [by the competitor]. After Amazon successfully induced the other online store to raise its price, Amazon continued to sell the product at the now-inflated price.

Project Nessie generated enormous profits for Amazon even though its higher prices caused Amazon’s unit sales to decrease. But in 2019 when regulators started snooping around, the company put Project Nessie on hold.

This will be a long, complicated case, and it is anyone’s guess how it turns out and if shoppers ultimately will see lower prices in the marketplace as a result of real competition.

Note to Readers: Although this story revolves around changes to particular Medicare health insurance plans, the lesson it offers is universal. During open enrollment, don’t just automatically renew your old plan. Look for changes your insurer is implementing in the coming year in the Annual Notice of Changes and see if a different plan may better suit your needs.

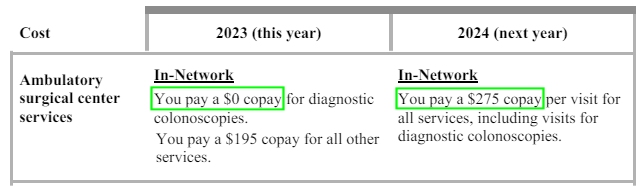

Here’s an example of a nasty change by Arkansas BlueMedicare. Their Premier Choice advantage plan used to provide free diagnostic colonoscopies, but for 2024 they added a $275 copay.

*MOUSE PRINT:

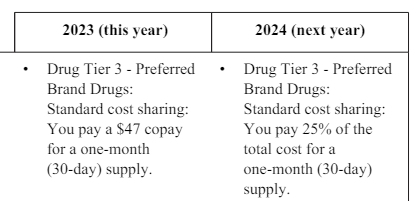

A very popular Medicare Part D drug plan is Wellcare Value Script (PDP). This is optional coverage for those with original Medicare whether or not you also have a supplement (medigap) plan. (Original Medicare does not cover drugs so many seniors buy a separate drug plan called Part D.)

A reason it is so popular is that it tends to be the cheapest plan in some states. For 2024, for example, in Massachusetts, Maine and perhaps elsewhere, the monthly premium is only 50 cents! In some other states it is zero!

It does have the maximum allowable deductible — $545 — but beneficially it does not apply to tier 1 or 2 drugs. Tier 1 has no copays, and tier 2 is only $5 or $15 for 30 or 90 days, respectively. But there is a big change for tier 3 drugs.

*MOUSE PRINT:

For 2023, there was a flat $47 or $44 copay for tier 3 drugs. That means whatever the full cost, you only had to pay forty-something dollars.

But, for 2024, that changes to co-insurance. To MrConsumer, “co-insurance” is a dirty word. It is cost-sharing between you and your insurance company. They pay part of a particular bill, and you pay a certain percentage of it. For 2024, you will pay 25-percent of the full cost of drugs in the Wellcare plan for that tier. If it is an expensive drug, you could get soaked. If it is a cheap drug, you could save compared to 2023. Note that some other copays are lower for 2024 on this Wellcare plan.

Now it’s time for you to fess up.

The bottom line is EVERY YEAR you really need to check and compare the features and costs of your current plan with what various of next year’s plans offer. This goes for regular insurance plans and any of your Medicare plans — Advantage, Supplement, or Part D (drugs). Remember to also check the drug formulary for changes to what drugs are covered, in which tier they reside, and what any restrictions are.

The FTC and 17 states recently

The FTC and 17 states recently