A Massachusetts credit union is advertising what appears to be a great rate on savings accounts — 4% interest. On top of that, they promise rewards for every debit card purchase, and to reimburse you for other banks’ ATM fees.

How can this little credit union beat the big online banks? The simple answer is they can’t.

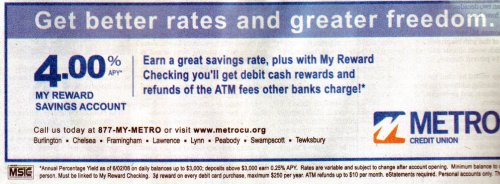

*MOUSE PRINT:

![]()

Only 0.25% interest on amounts over $3000? Thanks for nothing. If you make any sizeable deposit over $3000, your effective rate of interest will be far below the big online banks. (HSBC, for example, is paying 3.50% interest on up to $2,000,000 in deposits, until August 15.)

We won’t even get into the other fine print that requires that you also open a checking account, and only get back three cents per purchase as a reward.

I guess they’ll defend themselves with the argument that $3000 is a lot more than the average American can and will save, so their limitation is not ridiculous.

There are plenty of fine-print checking and savings accouts these days. But I’ll agree that the 3000 cap is extremely low.

Although, HSBC is paying 3.50% interest on up to $2,000,000 in deposits? Only the first $100,000 is FDIC insured, so be careful with that!

Not all have unfavorable terms. My credit union, Northeast Credit Union, offers an account with a 4.00% APY plus divident rate of 0.50%. The requirements are plainly stated: “member must have an open checking account or open a checking account to be eligible for a Silver Lining Savings Account.” Minimum opening balance: $5.00. These variable rates may change after the account is opened. The only fee listed is an Inactive Fee of $3 “charged on a share account starting the 13th month of inactivity and continuing until there is no balance or money is escheated to the state”. however, “This fee does not apply to members under 18, members with loans or IRA’s or any member with aggregated deposits over $200.”

I couldnt find any reason not to open the account. But I am aware that the rate only applies to the first $500 on deposit. It’s a nice way to gain a little interest on money I would put away for emergencies anyway.

It’s a good rate, and for most people it’s even a high enough limit that they will get that rate on all of their money. It’s just too bad they felt they needed to hide the limit in the small print.

Sure, 3.5% is good on a $500 deposit. Hiding the fact that a deposit over $3,000 earns 0.25% speaks directly to the trustworthiness and transparency of Metro Credit Union. It gives you a feeling that you’re dealing with an used car salesman instead of a banker.

I just wonder if you can open multiple accounts to get that rate in all of them…

e.g. for the FDIC insurance (unless they changed the rules since the ’80s), you get it for an account for yourself, and separate for you (primary name) + spouse, and separate for you + child 1, and separate for you + child 2, but not separate for spouse (primary name) + you since that’s the same as you and spouse. That would insure you up to $400,000. But gosh, what will I do with my other $1.6 million?

I’ve had great experience with INGDirect.com (currently 3.4% APY on their Electric Orange savings account)…I did close my account with them recently only because WAMU now offers a 3.75% APY on their online savings account, and since I already bank with WAMU it’s just easier for me. There is no balance limit with either of these companies for their online savings accounts, you get these great rates regardless of your account balance. Anyhow, if you don’t bank at WAMU I recommend going to INGDirect.com which is open to anyone and can be linked directly to your checking account with any bank so that you can transfer money online. They’ve bee great to me, even when I called to close my account they were very pleasant. And I firmly believe in spreading the good word when I am treated so well because customer service in general seems to be less and less of a priority to bigger companies these days. The only downside is they do not have bank branches in the US (that I know of, that may have changed). So if you’re not used to online banking it might not be the right fit for you.