More and more online news sites seem to be blurring the line between bona fide news and stories that seem more like advertisements.

Last fall, we demonstrated how some Tribune newspapers published product reviews naming the “best” products in a particular but sometimes obscure category, while the publisher quietly earned a commission on the sale of each one shown. Making money may have been a big motivation behind the columns.

Now Business Insider, a popular online site featuring business news stories, is publishing some articles that seem more like promotions than news features.

For example, last week they published this story:

Starting in the second paragraph, the reporter touts Ally Bank and the 11 high-yield savings accounts that she has opened there:

I earn interest on the money that’s sitting in that account, and it feels like I won a prize every time I check it.

My husband and I have 11 high-yield savings accounts with Ally, and we wouldn’t have it any other way.

…

Ally’s online interface makes it easy to see how much I have saved for each goal, and how much I’ve earned in interest this year — currently $44.31.

Say what? You have 11 accounts at Ally and all you’ve made is a measily $44? (We wrote to the reporter to ask if all that was really true, but she did not respond.)

In the story, not a negative word is said about Ally. The reporter mainly extols the virtues of high-yield savings accounts and the one at Ally Bank, but ignores the fact that more than three dozen other banks tracked by DepositAccounts.com pay higher rates of interest on savings accounts than Ally does.

Toward the end of the story, there is an embedded advertisement. Can you guess what bank is being advertised there?

*MOUSE PRINT:

That fine print says that a company called SmartAsset has placed this ad and earns revenue from it, as one might expect.

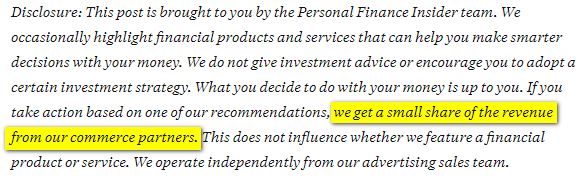

Business Insider then posts a disclaimer but only after the end of the story:

*MOUSE PRINT:

So Business Insider gets a cut of the commissions when readers open an Ally Bank account. Or perhaps 11 of them.

What is surprising is that back in October, Business Insider published two other similar pieces about Ally Bank where different reporters each touted their experiences with the same bank (and did not include criticism, nor any comparisons to other banks with high-yield accounts):

“I opened a high-yield savings account with online bank Ally to earn 20 times more on my money, and it’s safe to say I’m obsessed”

and

“I ditched my bank when I got married to earn 200 times more with an Ally high-yield savings account, and now I’d tell anyone to try it”

Exactly how many first person testimonial articles touting Ally Bank is Business Insider planning to publish? Could all these stories really be more about making money for Business Insider, Smart Asset, and Ally Bank rather than serving readers with a useful, objective analysis of high-yield savings accounts and the pros and cons of various providers?

Apparently a marketing theory gaining traction suggests that publishers can increase their their income by filling webpages with more “commerce content” — product-centric stories rather than traditional news stories or sponsored stories or ads. When viewers read these positive stories and if tracking reveals they bought the product or service, the publisher is compensated. According to one company in this business, Skimlinks, the most advanced publishers can derive 25-percent of their revenue this way.

The problem for readers is poor disclosure. Publishers should be upfront and disclose financial ties right at the top of stories, so we can better distinguish articles designed to sell us stuff from conventional editorial content.

The Federal Trade Commission (FTC) has two sets of guidelines that call for clear and conspicuous disclosure — one when commercial content is made to look like conventional editorial content (Native Advertising Guidelines) and the other when there is a financial connection between a presenter of information and the subject of that information (Endorsement and Testimonial Guidelines).

We asked all the parties involved (Business Insider, Ally Bank, and Smart Asset) to explain what’s going on here. Are these bona fide news stories or advertisements? Who provided the story and who is paying whom? And do any of them think that readers are being put on clear notice of the underlying commercial nature of them?

Business Insider did not respond directly, but through SmartAsset provided this statement:

Business Insider’s personal finance reporters covered Ally as a product they would recommend, which is their standard practice. In lieu of affiliate links which are common when it comes to “commerce content,” SmartAsset was used to sell ads against these stories. Any ad revenue generated by such coverage occurred independently of and only after the reporters’ decision to write about Ally.

For its part, SmartAsset (the company which placed the Ally ad), said it did not write the stories, nor pay Business Insider to write them. It only shares revenue with them.

Lastly, Ally Bank said it was not aware of the three stories above before they were published. It says it neither paid Business Insider nor SmartAsset to run them. It does pay SmartAsset to list its deposit rates on various websites.

So, what’s a savvy reader to do? Look more closely at content (stories, blog posts, etc.) even on respected news websites. Ask yourself why is this being posted? Is it truly conveying objective information, including both pros and cons? Are other competing products or services compared? Is there an ad or link within the content directly related to the subject of the story? Are there any disclosures that might reveal a hidden financial connection?

For our part, we will be bringing the concepts and issues related to “commerce content” to the attention of the FTC as they explore what changes should be made to their testimonial guidelines. You can participate in their process here.