Earlier this spring the Boston Red Sox announced a number of improvements to Fenway Park including that the venerable sport stadium was going cashless. That means if you want one of those famous Fenway franks or a beer or a souvenir you are going to have to pay with a credit or debit card.

Immediately MrConsumer knew that something was amiss here because Massachusetts law requires all retail establishments to accept cash.

*MOUSE PRINT:

No retail establishment offering goods and services for sale shall discriminate against a cash buyer by requiring the use of credit by a buyer in order to purchase such goods and services. All such retail establishments must accept legal tender when offered as payment by the buyer. — MGL c.255D, Sec. 10A

A number of states and cities have similar laws. It is often argued that the basis for this requirement is to prevent discrimination against the poor and minority groups that are more likely to be unbanked or underbanked. Despite the law, and apparently with only a cursory review, the Massachusetts Attorney General blessed this payment scheme after the Red Sox had already implemented it.

Federal law does not require the acceptance of cash irrespective of the “legal tender” language on our paper money.

At Fenway, three ReadyCARD kiosks have been installed to serve the one in 10 people who traditionally pay with cash. At these machines, those without a credit or debit card can insert cash ($5 minimum) and out pops a debit Mastercard. According to Red Sox management, there is no charge for the card. The card can then be used to pay for anything at the ballpark or anywhere else that Mastercard is accepted. The card is not refillable.

Demonstration of similar machine from the same company

MrConsumer suspected there were some hidden charges and other issues with these cards, but getting that information has proven almost impossible. Multiple requests to the Red Sox PR folks went unresponded to. Strike one. Multiple requests to Ready Credit Corporation, the provider of the reverse ATMs, also went unresponded to except for a terse statement advising us to contact the Red Sox because they themselves “don’t reply to media requests.” Strike two.

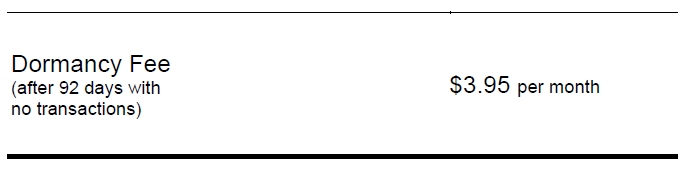

However, piecing together information gathered from Ready Credit’s website and one email from a Sox executive, prospective purchasers of these cards might be surprised to learn that there appears to be a $3.95 monthly “dormancy fee” automatically deducted from the card’s balance after just 92 days of non-use. [While Ready Credit would not confirm that this charge is from the applicable card agreement for the Fenway card, it appears to be.]

*MOUSE PRINT:

This is a big deal since you may not get full value for the cash you put on the card because of both the monthly fee and the general difficulty of using up small balances on any prepaid card.

Let’s say you have $8.12 left on the card and you want to buy a $10 item. Most online sellers don’t allow you to use a second debit or credit card to pay for the difference. (Amazon will allow you to transfer any remaining balance to your Amazon account, however.) Alternatively, you would have to find a retailer that will accept multiple forms of payment in one transaction known as a “split tender.” And if none of those options works for you, after a few months, don’t worry, the monthly fee will kick in, and the card’s balance will be wiped clean automatically in no time.

Under the Consumer Financial Protection Bureau’s (CFPB) relatively new rules, most vendors of prepaid cards have to disclose the costs of any card before purchase. It is unclear how reverse ATMs do this at Fenway Park, but the one above requires users to press an onscreen “terms and conditions” button to learn full details.

*MOUSE PRINT:

And even if you don’t click it, in fine print it says you have automatically agreed to the terms by buying a card or checking your balance.

Because of the unusual nature of these reverse ATM machines, and their location inside a private venue, the CFPB declined our request to confirm that the agency’s prepaid card rule actually applies in a case like this (although it probably does). And one of the most important provisions of that law prohibits card issuers from imposing a dormancy fee until the card has not been used for at least a year. Remember, this card charges a fee after just 92 days. Strike three.

So, we struck out in getting the full inside story about these cards. But, if you have used one of these machines at stadiums around the country, please tell us your experience in the comments below, and include if fees were disclosed to you prior to purchase.

Massachusetts Attorney General Maura Healey reached in warp speed her decision that the Red Sox cashless system was legal. The oh-so-likely backstory here is that Healey did not want to offend Red Sox owner John Henry in her run for governor. The same holds true for Bob Kraft, owner of the New England Patriots, which also uses a cashless system.

Healey refers to her office as “The People’s Law Firm.” Not in this case, Maura!

I absolutely disagree with her decision in regards to this, but I also understand why it’s not the hill she wanted to die on. This was a lose/lose situation for her no matter what she did.

Politics rules…money talks…fairness goes out the window…

This is disgusting for so many reasons.

It really overwhelmingly punishes the poor, over complicates what should be a very simple transaction (what happens in a network or power failure situation?), produces additional garbage for the landfill (not only the single-use cards but eventually the machines themselves will also end up there), and almost certainly is less accessible for those with mobility issues (who wants to travel an extra 100 feet for a hotdog?).

Just terrible.

Maura Healy is gutless. If you buy a $ 20.00 card there is no chance that your transaction will equal that exact amount so you lose the balance. I don’t care if Putin is running against her, she will not get my vote.

Please let’s move on from the political comments and attacks, and dwell on the primary issue here of how these reverse ATM cards may cause you a loss of money with some charges that may or may not have been disclosed clearly.

[edited] Ignore the truth? This mess is all greed and politial.

Parsing the MGL section “… requiring the use of credit….”

Aren’t the machines dispensing debit cards? So, it would seem Fenway is not in violation.

Edgar replies: Matt, but the law also says they must accept cash and a debit card is not cash.

One might argue that they ARE accepting cash (albeit only at the machines).

Seems that’s how they are skirting what appears to be the law’s intent.

This is gross negligence on the enforcement side of the government as there can be no reasonable belief that forcing customers to buy a debit card is in line with the spirit or text of the MA law that requires businesses to accept cash as a legal tender. This looks like Ready Station probably approached the Red Sox and offered a partnership to get this set up. This is pure profiteering off of customers who prefer to pay cash.

What happens if I put $5.00 on a card, spend $4.98, then toss the card with a balance of two cents? How will they collect $3.95 each month from me? I see having to first insert a Government ID card to purchase the debit card in the near future! Just my 2 cents worth!

Great point.

Based on the video posted all you do is plop in some money to the machine and get a card out. Based on what is left in the card they would only get 2 cents as they do not know who owns the card.

I’ll bet that the terms and conditions that you are ‘forced’ to accept are the standard 5-10 page of legal disclaimers that you couldn’t read even if you wanted to. There is probably a line behind you because they want to see the game and buy the local version of “Dodger Dogs” (I’m from Los Angeles.

Would you be able to download the T’s & C’s to a home email so that you can see exactly how you’ve been screwed?

Bob… I don’t think you can download anything from the machine. At RCBalance.com one can read the cardholder agreements… but there are about a dozen there.

What a horrible decision and precedent. Does the machine at least spit out a receipt? If so, I’d be keeping mine for the eventual Class Action to recover these punitive dormancy fees.

Edgar, you might’ve opened the political comment can of worms here when you mentioned the ‘cursory review’ by Maura Healy.

As others have mentioned, there’s no way she was going to rule against Mr. Henry et AL.

God help the people of the Commonwealth if she’s elected. I’m done.

Cedar Point here in Sandusky Ohio is doing the exact same thing. Same “dormancy fee” applies.

Is this the slow roll of the cashless society to come? Or just another way for these places to make a buck. We must not accept this.

https://www.cedarpoint.com/cashless

Why is the park going card-only or cashless?

By going cashless, we are able to conduct contact-less transactions, and it’s faster, safer and always secure.

_____________________

That is good for us but why throw in the 3.95 dormancy fees and why make these cards a one time fill only as well??

The purpose of the dormancy charge is to let the card expire. They don’t want to deal with thousands of 47 cent balances forever.

I don’t see a problem with the process. Unlike events where you need to use “tickets” to buy food, you *can* recover the balance from the card. Personally, I’d like to see it refillable, like many transit cards.

I disagree, Robert. The purpose of the dormancy charge is profit. If if was to let the card expire, they could do that without “stealing” the buyers’ money. It would be interesting to follow where the thousands of dollars in dormancy charges goes. Do the venues get a cut?