About 10 states require sellers of gift cards to refund small balances of money left on previously used cards. So if a $50 card only has $4.82 left on it, you can ask for that money back. The trouble is, some gift card sellers, like Dunkin’, are allegedly refusing to make those refunds.

So earlier this month, a New Jersey consumer sued Dunkin’ in its home state of Massachusetts on behalf of all customers who have been refused refunds (see complaint).

The complaint alleges that Dunkin’ has no mechanism for making these refunds when a customer requests it despite language on its cards that says:

*MOUSE PRINT:

“Card Value may not be redeemed for cash, check or credit unless required by law [emphasis added].

Under the laws of both Massachusetts and New Jersey, when a gift card’s balance is below $5 (MA is $5 or less), upon request, the merchant must refund the balance.

*MOUSE PRINT:

A purchaser or holder of a gift certificate … which has been redeemed in part, such that the value remaining is $5.00 or less, shall make an election to receive the balance in cash or continue using the gift certificate. — M.G.L.A. 200A § 5D

[I]f a stored value card is redeemed and a balance of less than $5 remains on the card after redemption, at the owner’s request the merchant or other entity redeeming the card shall refund the balance in cash to the owner. — N.J.S.A. 46:30B-42.1(h)

The court case alleges that Dunkin’ has been unjustly enriched by pocketing all the remaining balances on cards, and is in breach of various consumer protection laws in addition to the gift card statutes. Dunkin’ did not respond to multiple requests for comment.

It will be interesting to hear what imaginative defense Dunkin’ comes up with, or perhaps it will just quickly settle the case.

Earlier this spring the Boston Red Sox announced a number of improvements to Fenway Park including that the venerable sport stadium was going cashless. That means if you want one of those famous Fenway franks or a beer or a souvenir you are going to have to pay with a credit or debit card.

Immediately MrConsumer knew that something was amiss here because Massachusetts law requires all retail establishments to accept cash.

*MOUSE PRINT:

No retail establishment offering goods and services for sale shall discriminate against a cash buyer by requiring the use of credit by a buyer in order to purchase such goods and services. All such retail establishments must accept legal tender when offered as payment by the buyer. — MGL c.255D, Sec. 10A

A number of states and cities have similar laws. It is often argued that the basis for this requirement is to prevent discrimination against the poor and minority groups that are more likely to be unbanked or underbanked. Despite the law, and apparently with only a cursory review, the Massachusetts Attorney General blessed this payment scheme after the Red Sox had already implemented it.

Federal law does not require the acceptance of cash irrespective of the “legal tender” language on our paper money.

At Fenway, three ReadyCARD kiosks have been installed to serve the one in 10 people who traditionally pay with cash. At these machines, those without a credit or debit card can insert cash ($5 minimum) and out pops a debit Mastercard. According to Red Sox management, there is no charge for the card. The card can then be used to pay for anything at the ballpark or anywhere else that Mastercard is accepted. The card is not refillable.

Demonstration of similar machine from the same company

MrConsumer suspected there were some hidden charges and other issues with these cards, but getting that information has proven almost impossible. Multiple requests to the Red Sox PR folks went unresponded to. Strike one. Multiple requests to Ready Credit Corporation, the provider of the reverse ATMs, also went unresponded to except for a terse statement advising us to contact the Red Sox because they themselves “don’t reply to media requests.” Strike two.

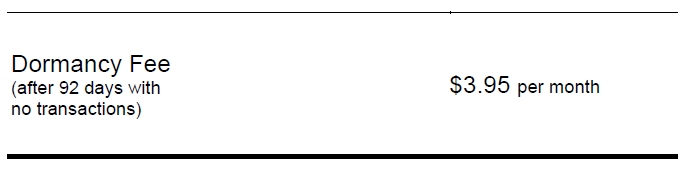

However, piecing together information gathered from Ready Credit’s website and one email from a Sox executive, prospective purchasers of these cards might be surprised to learn that there appears to be a $3.95 monthly “dormancy fee” automatically deducted from the card’s balance after just 92 days of non-use. [While Ready Credit would not confirm that this charge is from the applicable card agreement for the Fenway card, it appears to be.]

*MOUSE PRINT:

This is a big deal since you may not get full value for the cash you put on the card because of both the monthly fee and the general difficulty of using up small balances on any prepaid card.

Let’s say you have $8.12 left on the card and you want to buy a $10 item. Most online sellers don’t allow you to use a second debit or credit card to pay for the difference. (Amazon will allow you to transfer any remaining balance to your Amazon account, however.) Alternatively, you would have to find a retailer that will accept multiple forms of payment in one transaction known as a “split tender.” And if none of those options works for you, after a few months, don’t worry, the monthly fee will kick in, and the card’s balance will be wiped clean automatically in no time.

Under the Consumer Financial Protection Bureau’s (CFPB) relatively new rules, most vendors of prepaid cards have to disclose the costs of any card before purchase. It is unclear how reverse ATMs do this at Fenway Park, but the one above requires users to press an onscreen “terms and conditions” button to learn full details.

*MOUSE PRINT:

And even if you don’t click it, in fine print it says you have automatically agreed to the terms by buying a card or checking your balance.

Because of the unusual nature of these reverse ATM machines, and their location inside a private venue, the CFPB declined our request to confirm that the agency’s prepaid card rule actually applies in a case like this (although it probably does). And one of the most important provisions of that law prohibits card issuers from imposing a dormancy fee until the card has not been used for at least a year. Remember, this card charges a fee after just 92 days. Strike three.

So, we struck out in getting the full inside story about these cards. But, if you have used one of these machines at stadiums around the country, please tell us your experience in the comments below, and include if fees were disclosed to you prior to purchase.

With egg prices going through the roof at the moment, some companies still promote premium-priced eggs because they are seemingly raised in a more humane way such as those that are “cage-free” or “free range.”

One such company, Nellie’s, sells Free Range eggs and claims in this video that unlike other egg farming factories that house their hens in overcrowded warehouses…

“Our free-range hens get to live their lives like real hens, with access to pasture everyday in good weather. Our hens can spread their wings, forage in the fields, or scratch in the dirt.â€

Even on their [previous] box, the company claims that their chickens “get to peck, perch, and play on plenty of green grass.”

But, a class action lawsuit says that a more accurate depiction of the everyday conditions Nellie’s hens face is this, taken from a PETA video:

*MOUSE PRINT:

The complaint alleges:

… the conditions in Defendant’s henhouses are virtually indistinguishable as those from the example they show as being not “Free Range†where hens are essentially “liv[ing] inside a space much like a large overcrowded warehouse.†Nellie’s itself describes this as a “grim existence†for these hens. But contrary to its packaging representations, that is precisely how Nellie’s own hens live.

Defendant’s hens can only get outside through small hatches cut at intervals along the sides of the shed. The hatches are closed all winter and during inclement weather. In pleasant weather the hatches are closed at night and are not opened until 1 pm the next day.

Because of this overcrowding and limited time that the hatches are open, many of Defendant’s hens are unable to ever access the hatches or the outdoor space.

The lawsuit, therefore, alleges false and misleading claims are being made by the company. A couple of months ago, a judge denied the company’s motion to dismiss the case. Here is a little more about the case and the judge’s initial ruling.

Godiva Case Update

Back in December we told you about a class action case filed by consumers against the Godiva chocolate company for misleading customers into believing that their expensive delicacies were made in Belgium when in fact they are manufactured in Pennsylvania. (See our original story.)

Now a judge has approved a negotiated settlement between the parties giving consumers who purchased Godiva products between 2015 and 2021 up to a $25 refund with proof of purchase. Several state AGs objected saying the terms of the settlement did not benefit consumers enough, but the judge denied their claims. Oddly, the deadline for filing claims passed before the judge made his final ruling.

About 10 states require sellers of gift cards to refund small balances of money left on previously used cards. So if a $50 card only has $4.82 left on it, you can ask for that money back. The trouble is, some gift card sellers, like Dunkin’, are allegedly refusing to make those refunds.

About 10 states require sellers of gift cards to refund small balances of money left on previously used cards. So if a $50 card only has $4.82 left on it, you can ask for that money back. The trouble is, some gift card sellers, like Dunkin’, are allegedly refusing to make those refunds.

With egg prices going through the roof at the moment, some companies still promote premium-priced eggs because they are seemingly raised in a more humane way such as those that are “cage-free” or “free range.”

With egg prices going through the roof at the moment, some companies still promote premium-priced eggs because they are seemingly raised in a more humane way such as those that are “cage-free” or “free range.”